Let's be honest for a second. We've all seen the videos on YouTube, Instagram, or TikTok—someone typing on a Macbook from a pristine beach in Bali, selling the ultimate modern fantasy: Passive Income.

They suggest that if you just buy their course or follow their simple framework, you can set up a business in an afternoon, press a few buttons, and wake up every single morning to thousands of dollars quietly deposited into your bank account while you slept. They pitch the idea that the link between your time and your money can be effortlessly severed if you just know the "secret".

While passive income is a very real and powerful concept, the way it is often portrayed online is an illusion that glosses over the hard work required to build it.

I am here to give you the harsh, unglamorous, and deeply uncomfortable reality check about passive income. Passive income is not a myth—it is absolutely real. But the way it is sold on the internet is a catastrophic misrepresentation of the sheer, unadulterated suffering required to build it.

I want to strip away the marketing jargon and talk about the raw mechanics of detaching your time from your income. Because the truth is, unless you have a massive trust fund or you win the lottery, generating true passive income requires an incredibly violent and active upfront sacrifice.

Let me tell you about my personal journey with this, why I am actively pursuing it despite the pain, and the absolute reality of how income actually works.

The Great Irony of My Nomadic Journey

Let's start with full transparency: I am currently making passive income.

However, let me be explicitly clear so you don't misunderstand my position—the passive income I generate is not enough to live on.

While I could technically start selling off pieces of my investments to make up the difference and fund my travels, I do not want to do that just yet. I am young, and the compounding runway ahead of my portfolio is far too valuable.

So, sitting on this realization—that the current passive yield isn't enough to live on on its own—I simply want to increase my passive income streams.

About a year ago, I made a massive life pivot. I started a nomadic journey.

Prior to this, my entire financial thesis was based on the standard, societal default: exchanging my deeply finite time for a W-2 salary route. I gave an employer 40 to 60 hours of my vital life energy every week, and in exchange, they gave me a direct, linear payout. It was an active job. It was safe. It was predictable. But it was a fundamental trap.

When I packed up and initiated this nomadic existence, my core objective was to aggressively pivot away from that active exchange. My thesis was that I wanted to invest my raw, unstructured time into creating digital assets—things that could scale infinitely and eventually detach my physical labor from my financial reward. I wanted to build the very thing I had been reading about for years.

It has been exactly one year of relentlessly pursuing and learning how to actually do this.

What is the verdict after 365 days?

The good part is that it has been incredibly exciting. Waking up every day with sovereign control over your schedule, staring at a blank screen, and trying to build something out of absolutely nothing is intellectually exhilarating. It forces you to grow in ways a corporate cubicle never could.

But the bad part? The deeply sobering, agonizing truth?

Making passive income is brutally, mercilessly hard.

And herein lies the great irony of my current life: I am currently working harder, longer, and more actively than I ever have in my entire life, entirely for the purpose of trying to make "passive" income. I am actively stressing, actively grinding, and actively solving complex problems every single day just to build systems that might, eventually, pay me while I sleep.

This grueling year has completely shattered my preconceived notions. It has made me realize that passive income is sold on the internet the wrong way. It is sold as a shortcut. It is actually the longest, steepest, most treacherous path up the mountain.

To understand why, we need to completely deconstruct how money is made. We need to categorize the ecosystem.

I want to decisively divide the world of money into Four Types of Income. If you understand these four categories, you will be immune to the internet charlatans, and you will understand exactly what it actually takes to buy your freedom.

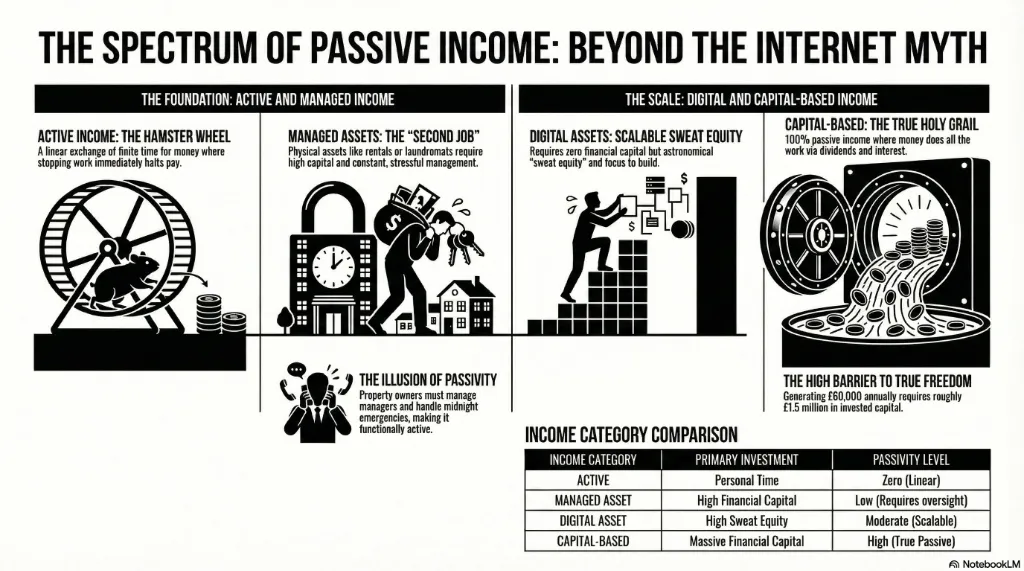

Income Type 1: Active Income (The Hamster Wheel)

This is the baseline. This is where 99% of the global population operates. Active income is the most conceptually simple transaction in human history: you trade your physical time and manual effort for an agreed-upon amount of money.

You work for an hour; you get paid for an hour. You stop working; the money stops coming in.

There is zero ambiguity here. If you are a bartender, a software engineer at a FAANG company, a corporate lawyer, or a freelance graphic designer, you are generating active income. Yes, the corporate lawyer might charge $800 an hour while the bartender makes $15 an hour plus tips, but the underlying mechanical physics of their income are identical. If either of them gets sick, takes a three-month sabbatical, or decides to just stay in bed on a Tuesday, their income immediately drops to zero.

The psychological safety of Active Income is incredibly seductive. You know exactly what is going into your bank account every two weeks. It allows you to plan your life, sign a lease, taking out a car loan, and feel secure.

But the fatal flaw of Active Income is that it is fundamentally capped by your biology. There are only 24 hours in a day. You have to sleep. You have to eat. No matter how much you optimize your productivity, no matter how many promotions you beg for, you will mathematically hit a ceiling of earning potential because your time is finite.

To escape the Hamster Wheel, you have to transition to the other three types of income. But as you are about to see, none of them are free.

Income Type 2: Managed Asset-Based Income (The Second Job)

This is the category that most people mistakenly label as "passive income." This includes owning real estate (like residential rental properties or commercial buildings) and purchasing or building small physical businesses (like a laundromat, a car wash, or a local service company).

Let's look at the mechanics here.

In Managed Asset-Based income, the required upfront financial investment is typically exceptionally high. You need a $60,000 down payment for a duplex, or you need to secure a $250,000 small business loan to buy the neighborhood car wash.

Because the capital risk is immense, the financial returns can also be extremely high. Real estate leverages debt to amplify returns, and small businesses can generate massive localized cash flow. Furthermore, there is a slight, tangible disconnect between your direct, hour-by-hour work and the income generated. If you own a duplex and sleep for eight hours, your tenant is technically paying you rent while you sleep.

But here is the brutal reality: It is not, in any functional sense, fully passive.

Managed Asset-Based income realistically requires constant, low-level anxiety and periodic intense intervention. It is essentially a second job.

If you own a rental property, you have to ensure the physical integrity of the structure. When the hot water heater explodes at 2:00 AM on a Sunday, your "passive" income suddenly requires you to frantically call emergency plumbers and bleed thousands of dollars in cap-ex repairs. You have to manage property managers (who often require as much managing as the properties themselves). You have to deal with tenant evictions, local zoning laws, and fluctuating property taxes.

If you own a car wash or a laundromat, machines break. Employees quit without notice. Vandalism occurs.

There are always things that physically need to be ensured. The asset demands to be managed. While you are severing the direct "hourly wage" connection, you are replacing it with a heavily capitalized management role. It is a fantastic way to build immense wealth, but do not fool yourself into thinking you can simply sit on a beach and ignore a managed physical asset. It will decay, and your income will vanish.

Income Type 3: Digital Asset-Based Income (The Scalable Sweat Equity)

This is the arena I am currently bleeding in. This is the core of my nomadic journey.

Digital Asset-Based Income encompasses writing articles (like this one), coding applications, building software-as-a-service (SaaS) websites, painting digital art, creating YouTube videos, or building massive online audiences.

The mechanical structure of this income is entirely unique. Unlike Managed Assets (which require massive upfront capital), the investment required for Digital Assets is extremely low in terms of dollars, but astronomically high in terms of raw time, sweat equity, and intense focus.

You do not need a $50,000 bank loan to sit at your kitchen table and write a sprawling 3,000-word essay, or to learn Python and build an app over six months. The barrier to entry is virtually zero. Because the barrier to entry is zero, the competition is virtually infinite.

The allure of the Digital Asset is its scalability. Once I write a highly optimized piece of code or publish a universally helpful article, it costs me exactly $0.00 to distribute that asset to one person, or to one million people. A piece of software can be sold endlessly without ever running out of inventory. The decoupling of time and money here is the most dramatic of any income type: you might spend 400 grueling hours building an app that makes absolutely nothing, and then in hour 401, it goes viral and generates $50,000 in a weekend.

But this is exactly what the internet gurus completely misrepresent.

Building a digital asset that actually generates meaningful revenue is a brutal, psychologically taxing grind. It requires you to work in the dark, often for years, with absolutely zero financial positive reinforcement. When you are writing code at midnight on a Friday, no boss is paying you overtime.

And even when you finally succeed, Digital Assets are notoriously fragile. Technology changes. Google updates its search algorithm and wipes out your blog traffic overnight. A competitor clones your app and releases it for free. To keep a digital asset generating income, you have to constantly update it, market it, and defend it.

It is "passive" only in the sense that the asset handles the transaction while you sleep. But building and defending the asset requires a monumental, highly active crusade.

Income Type 4: Capital-Based Passive Income (The True Holy Grail)

Finally, we arrive at the only category of income on earth that is actually, definitively, 100% passive: Capital-Based Passive Income.

This includes dividend-paying stocks, broad-market index funds (like the S&P 500), municipal bonds, High-Yield Savings Accounts (HYSAs), and peer-to-peer lending portfolios.

In this scenario, your money is literally doing all of the work. You deploy capital into complex, global economic machines, and you walk away. When you buy an index fund, millions of employees at the 500 largest companies in America wake up, commute to work, stress over spreadsheets, innovate, and maximize profits. You simply sit there, do absolutely nothing, and capture a microscopic fraction of their collective global output in the form of capital appreciation and dividends.

If you have a million dollars in a high-yield savings account earning 5%, you will be handed $50,000 every single year. You don't have to fix a toilet. You don't have to update thousands of lines of code. You don't have to market a product. You just wait.

It is pure, unadulterated financial perfection.

But there is a massive, crushing caveat.

For Capital-Based Passive Income to generate a meaningful, life-sustaining amount of money, the upfront capital required must be incredibly high.

Returns in this category are mathematically tethered to macroeconomic reality. You cannot consistently generate 40% annual returns without taking on catastrophic risk. Safe, predictable capital returns generally hover in the 4% to 8% range above inflation.

Therefore, if you want to generate $60,000 a year of truly passive income to live on, you need roughly $1.5 million in invested capital.

That is the wall that everyone hits. They love the idea of sitting back and collecting dividends, but they mathematically cannot stomach the decade of grinding active labor required to build a $1.5 million portfolio. They want the returns of the Capital Class, but they only possess the leverage of the Laborer.

Returns here will generally be less than the explosive potential of building a business or an app. They can be more, of course, if you get wildly lucky with an individual stock pick, but you cannot guarantee that at all. The beauty of Capital-Based income is not its speed; it is its terrifying, compounding inevitability over long periods of time.

The Blueprint: Synthesizing the Path Forward

When you look at these four categories stripped of their marketing hype, the truth becomes painfully clear. Financial freedom is not a hack you can buy for $997. It is a long, deliberate sequencing of different active sacrifices.

Everyone wants to jump straight to the end. Everyone wants to immediately live off of pure Capital-Based income while currently sitting on a net worth of zero. The math does not, and will never, work that way.

If you are serious about achieving financial independence, you have to execute a structured, sequential blueprint. You have to move through the income types deliberately.

Here is what the actual path to freedom requires:

First, you have to embrace the active grind. You have to take a Type 1 Active Income job, push your earning potential as high as possible, and save an aggressive, almost painful portion of your salary. You are exchanging your time to stockpile ammunition.

What you decide to invest that stockpiled money in next depends entirely on your appetite for risk, your desired speed of returns, and exactly how "passive" you want your daily life to actually be.

If you want speed and high cash flow, and you are willing to manage headaches, you deploy that active cash into Managed Assets (Type 2). If you want total safety and zero physical effort, you deploy it into Capital Assets (Type 4), acknowledging that it will take 15 years to compound to a livable wage baseline.

But I want to share the specific, sequential path that I am currently on. My journey is not the only way, but it is the blueprint I have constructed to navigate this paradox.

Phase 1: Establish Capital-Based Passive Income

This is step one. Before you take any massive entrepreneurial leaps, you must build a bedrock foundation. You must execute the active grind and funnel that money directly into broad index funds and safe capital assets. The goal here is not to completely live off the dividends immediately. The goal is to build a massive, compounding engine in the background that serves as a financial safety net. Because when you attempt the harder phases of income generation, you inevitably fail multiple times. A strong capital baseline ensures you don't starve when you do. You save until you hit Coast FIRE or a robust portfolio size.

Phase 2: Build Digital Asset-Based Income

This is where I am right now on this nomadic journey. With my capital baseline compounding quietly in the background, I have stepped away from the traditional 9-to-5 active route. Instead of trading my time linearly for a salary, I am investing my thousands of unstructured hours into building highly scalable digital assets: writing, coding, software, and platforms.

This phase is intensely demanding. It requires massive sweat equity. It is low-friction in terms of hard cash outlay, which makes it perfect for a young person trying to keep their living expenses lean while traveling the world. The goal here is to eventually strike the nonlinear scalability of the internet.

Phase 3: Transition into Managed Asset-Based Income

This is the final stage. Once the digital assets mature and begin generating massive sums of cash, and the capital portfolios swell behind them, the strategy pivots toward diversification. This is when you take the significant, reliable cash flows generated by the digital empire and funnel them into physical, Managed Asset-Based income—syndicated real estate, brick-and-mortar cash-flowing businesses, and physical infrastructure.

At that point, the digital assets feed the managed assets, and the managed assets further bolster the capital baseline. The wheel turns on its own.

The Final Reality Check

Passive income is the most beautiful financial concept in the world, but it is a privilege that must be violently earned.

Stop looking for the secret button. Stop believing the teenagers selling lifestyle courses from a rented beach house. Understand the mechanics of what you are actually trying to build.

Whether you choose to grind away at a W-2 to buy index funds, deal with tenant plumbing disasters to build a real estate empire, or stare at a glowing screen at 3 AM debugging code to build a digital asset—you are going to suffer to generate your wealth.

The only choice you actually have is deciding which type of suffering aligns best with the life you want to live. Pick your suffering, drop the delusions, and get to work.