And how my ButFirstFIRE dashboard shows the math clearly

Most people underestimate how powerful small monthly savings can be. They think saving $500 a month is “nice,” but not life-changing. On the FIRE path, that number is a rocket booster. If you invest $500/month at a modest 7% annual return, you add roughly $120,000 in 10 years, $260,000 in 20 years, and over $570,000 in 30 years.

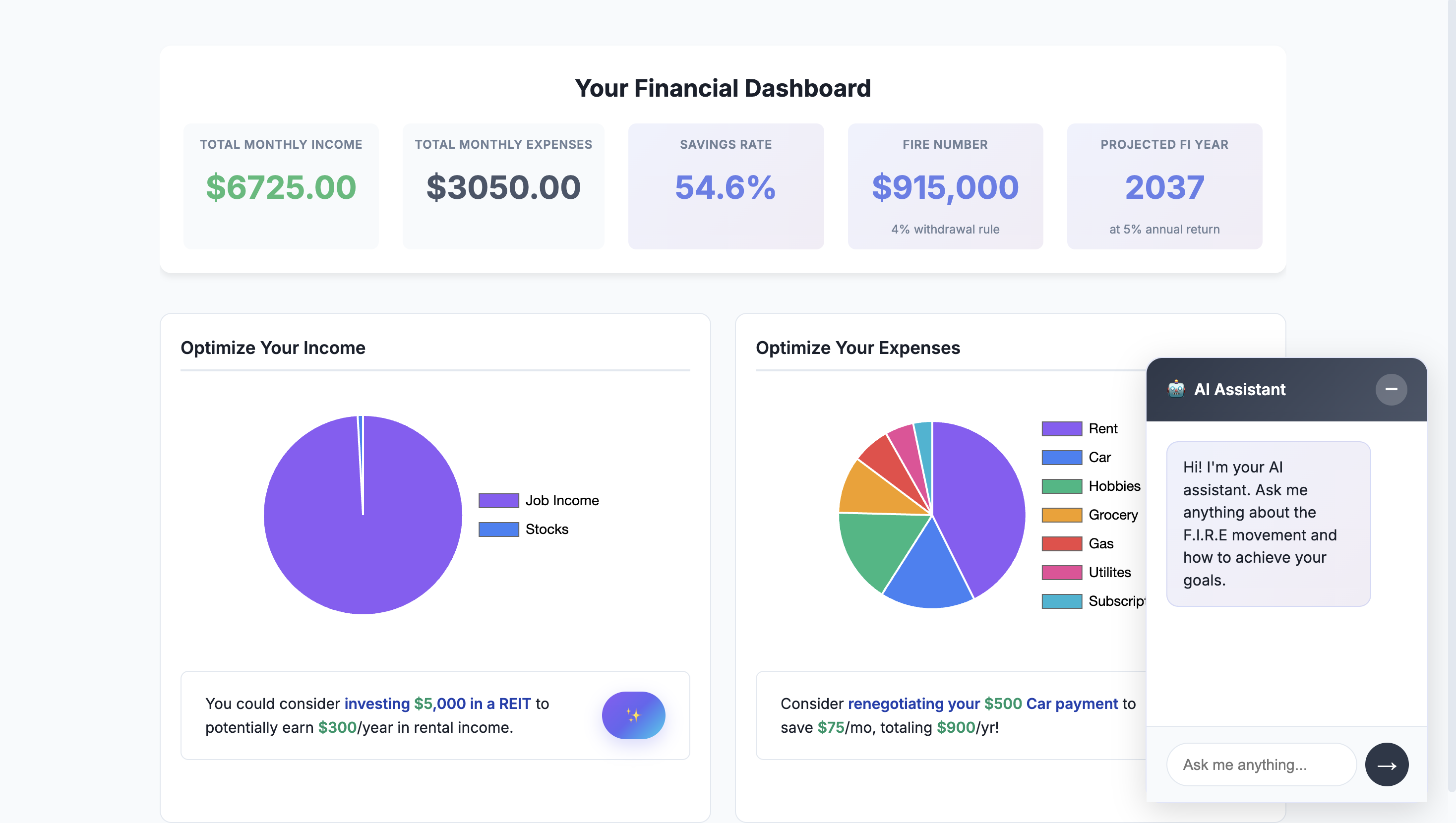

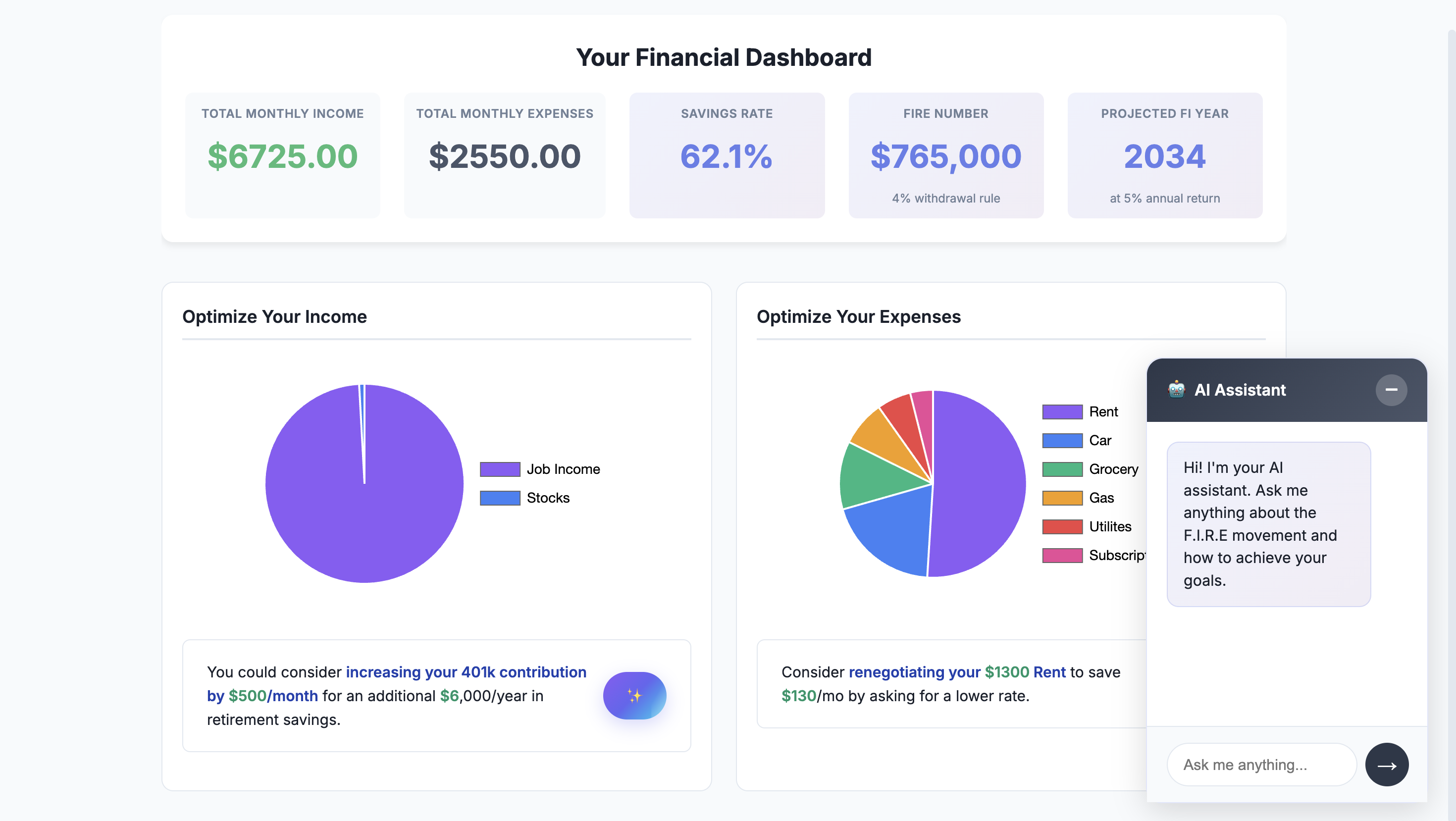

Take a look at the dashboard below to see how the extra $500/month can move your retirement date forward by 3 years depending on your income, lifestyle, and savings rate.

An average American making a modest $80k salary and spending around national averages can retire roughly 3 years earlier by using the rules below consistently.

If you’re currently saving 10% and jump to 20%, your FIRE timeline doesn’t speed up by 10%. It can speed up by Years. This is the magic of compounding combined with a higher savings rate.

On ButFirstFIRE, we break down your exact numbers — your income, your expenses, your FI number, and your projected retirement year — and show exactly how the extra $500 affects your timeline. The dashboard shows, in real time, how each spending habit pushes your FIRE date earlier or later.

The good news: getting to that extra $500/month doesn’t require extreme frugality. You don’t need to live like a monk, eat rice and lentils for eternity, or swear off joy. You just need structure, a few simple behavioral tricks, and some guardrails that make saving the default instead of the exception.

Below are six practical saving strategies that help you reliably hit that $500/month mark… and they don’t feel like punishment.

Key Takeaways

- Saving $500 a month equals $6,000 per year before investment growth.

- Invested consistently, $500/month can become roughly $260,000 over 20 years at a 7% annual return.

- You do not need one huge sacrifice. Six smaller rules can combine into a reliable $500/month savings gap.

- The FIRE benefit comes from two forces at once: lower annual expenses and more money invested.

1. One “No-Spend Day” Per Week

A no-spend day is not about deprivation. It’s about interrupting the constant stream of micro-purchases that bleed your wallet dry without you noticing.

How it works:

- Pick one day each week.

- No purchases — not even $4 snacks, not even $2 apps.

- Eat what’s already at home. Use what you already own.

Why it works:

Most unnecessary purchases happen in micro-moments of boredom or convenience. Removing one day a week can automatically cut:

- $40–$70 in random food spending

- $20–$40 in small apps, coffees, and impulse buys

Monthly savings: $60–$120

Annual impact: $720–$1,440

2. The “Add to Cart, Wait One Week” Rule

Impulse spending is the silent killer of FIRE progress. You think you’re making one-off purchases, but they snowball. This trick turns impulsivity into intentionality.

How it works:

- When you want to buy something → add to cart.

- Do not buy it for 7 days.

- Revisit it next week and decide if it still matters.

Why it works:

80% of impulse purchases lose their appeal within 72 hours.

The average person eliminates $100–$300/month of unnecessary items with this delay.

Monthly savings: $100–$250

Annual impact: $1,200–$3,000

FIRE acceleration: ~6–12 months earlier depending on your savings rate

3. The “No Uber Under 3 Miles” Rule

This rule is simple and brutal — but ridiculously effective.

How it works:

- If your destination is 3 miles or less, you don’t Uber.

- You walk, cycle, scooter, or take public transport.

Why it works:

Short-distance Ubers are the most expensive per mile.

They’re also usually the ones taken out of laziness, not necessity.

Cutting 10–15 short rides a month easily saves:

- $80–$150 for city-dwellers

- + improved health

- + more daily sunlight, which bizarrely improves financial discipline too

Monthly savings: $80–$150

Annual impact: $960–$1,800

4. Review Subscriptions Monthly

Subscriptions multiply quietly. You sign up for a $7 app here, a $14 trial there, a $20 upgrade next month — and suddenly you’re at $250–$400/month without noticing.

How it works:

- Have a “First Sunday Subscription Review.”

- Delete or downgrade three things every month.

- Keep the ones you truly use.

Why it works:

Subscriptions decay in value over time, but the billing doesn’t.

You’ll usually find:

- streaming you don’t watch

- apps you forgot about

- services you don’t need

- auto-renewals you never intended

Monthly savings: $40–$100

Annual impact: $480–$1,200

5. Buy a Coffee Maker (French Press or Moka Pot)

At ButFirstFire, we are huge fans of coffee ourselves. Hence the pun in the title. But coffee expenses add up fast. The $5 coffee quickly becomes a $7 coffee with tips and taxes and $10 if you can't resist getting the cookie as well. Coffee expenses therefore need to be watched.

How it works:

- Keep your café visits for social moments.

- Make everyday coffee at home.

- Use a French Press (link) for a rich, easy brew.

- Or go with a classic Moka Pot (link) for bold, espresso-style coffee at home.

Why it works:

You don’t quit coffee — you just shift the habit.

Most people save $60–$150/month with this alone.

Monthly savings: $60–$150

Annual impact: $720–$1,800

6. Marketplace Before Amazon, Refurbished Before New

Amazon is the easy button. They now have a one-click buy button. It's the doom of impulse buyers. But “easy” kills FIRE goals.

How it works:

Before buying anything new:

1. Search Facebook Marketplace

2. Check refurbished listings

3. Compare prices

4. Only buy new if necessary

Why it works:

You cut 30–70% off retail prices on:

- electronics

- furniture

- appliances

- gadgets

- hobby gear

Most people save $100–$200/month with this rule, without sacrificing quality.

Monthly savings: $100–$200

Annual impact: $1,200–$2,400

Putting It All Together

If you implement every rule aggressively:

- Minimum savings: ~$450/month

- Common savings: ~$600–$800/month

- Extreme but realistic: ~$1,000/month

Even the conservative $500/month savings gives you:

$6,000/year saved

$6,000/year invested

$6,000/year compounding

This alone can shift your retirement by several years earlier. Every $500 saved impacts your FIRE number significantly. And if you increase income simultaneously — even better, because the timeline shrinks dramatically when savings rate grows from 20% → 40%.

If you'd like to track your progress, you can use our ButFirstFIRE dashboard. It shows your exact numbers — your income, your expenses, your FI number, and your projected retirement year — and shows exactly how the extra $500 affects your timeline. The dashboard shows, in real time, how each spending habit pushes your FIRE date earlier or later.

This is where the journey becomes tangible, where the math stops being abstract and starts being motivating.

You don’t need a radical lifestyle overhaul. You don’t need to give up everything. You don’t need to live like it’s 1930.

You just need a handful of rules that nudge you toward intention instead of convenience.

And those rules — done consistently — can buy you something priceless:

years of freedom back. See how I saved 50% of my income in my journey to Coast FIRE at 33.